REIT Total Return Portfolio Heading into 4Q2022

A Dark 6 Years for REITs

The REIT Total Return Portfolio began trading on 7/1/16 and its 6.25 years of operation have been in one of the roughest REIT markets of all time.

They say to make hay when the sun is shining, but what are you supposed to do when it’s not?

I think you just make hay anyway.

Over 6.25 years the REIT index returned only 14.47%.

If we were to look at price alone, the REIT index is down 10.26%.

More than 100% of the return came from dividends.

Even in this dark period, there were opportunities to outperform the index. Certain portions of the REIT market were overhyped and had bloated valuations. Simply avoiding these names helped substantially. There were other pockets of the market that despite excellent fundamental setups were unpopular, affording us an opportunistic entry point.

Over this same time period, 7/1/16 – 9/30/22, we managed to capture a total return of 36.64%. That is far less than we would normally like to get in 6.25 years, but given that it was one of the worst 6.25 years in REIT history we are proud of the result.

Our active management is a continuous process of repositioning into high-quality undervalued REITs. Each trade individually is a small advantage, but they sum to a total return that was a bit more than triple the index return.

Goal and process of REIT Total Return portfolio

We do not chase exciting stocks or speculate. It is a simple matter of fundamental analysis informing stock selection. We are guided by an underlying philosophy that a diversified portfolio of stocks with a superior combination of quality and value will outperform over time.

As of 9/30/22 here is the diversification by economic exposure:

Superior quality and value are partially a matter of top-down sector selection. You may note in the pie chart above that we have 0 exposure to hotels, self-storage, and casinos. Hotels are fundamentally disadvantaged in their vertical with travel agencies and brands perpetually eating up too high a percentage of profits. Self-storage and casinos are perfectly fine sectors fundamentally but are getting a bit expensive on valuation.

We also have a massive underweight relative to the index in office as we think the sector is oversupplied with new construction still coming in despite high national vacancy rates.

In contrast, we are intentionally overweight sectors that have more growth and are undersupplied.

- Farmland

- Housing (apartments, homebuilding, and manufactured housing)

- Hospitals

- Labs

- Manufacturing facilities

- Fiberoptic cable

We also like towers but that is not an overweight because the tower REITs are a massive portion of the index.

Superior quality and value also come from individual stock selection within the 21 REIT property sectors.

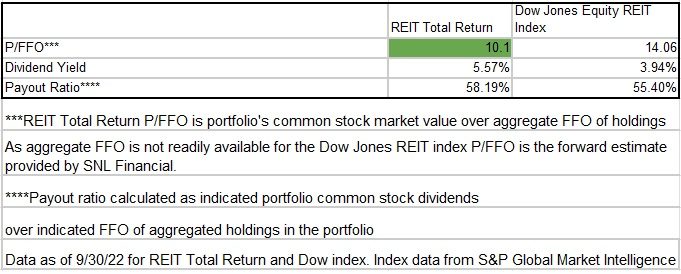

The REIT index has an FFO multiple of 14.06X while our portfolio has a multiple of 10.1X

That extra value means we have a cashflow yield of 9.9% while the index has a cashflow yield of 7.1%. More cashflows mean a bigger dividend yield at 5.57% while maintaining a reasonable payout ratio of 58% such that there is plenty of capital left over for growth.

Going forward – Spring-loaded portfolio

Having survived the dark times with a moderate return we look forward to working in a more favorable environment.

It is worth noting that this dark period is quite unusual for REITs as they have typically outperformed the market and delivered a CAGR of somewhere in the 9%-11% range depending on the time period. The 30-year chart, for example, shows a 1039% return.

This sharp contrast between recent REIT performance and long-term REIT performance lends itself to the question: Has something fundamentally changed that REITs are no longer a high return sector?

Market sentiment on real estate is so low right now that they seem to think this is the case, but there are 2 factors that we think suggest the good times will return

- Valuation

- Growth

While REIT prices have been down for 6.25 years, FFO/share has grown. REITs have also upped their quality with lower debt levels and have transitioned their portfolios to better asset types.

In combination, this makes REITs spring-loaded to bounce out of this dip.

The REIT index FFO multiple is now 14.06X as of 9/30/22. That is the cheapest it has been in quite some time.

When you have an investing universe that is both higher quality/growth than normal and trading at a lower multiple than normal, that is a recipe for much higher returns. We can’t predict exactly when sentiment will rebound or when the market pricing bottom will be, but the sheer fundamental strength relative to the price is phenomenal right now.

Evolving economies create opportunity

Our REIT Total Return Portfolio is actively managed to pivot into wherever the opportunity is greatest. We are now offering portfolio mirroring in which the trades in our REIT Total Return Portfolio are automatically executed in client portfolios simultaneously and at the same price.

Important Notes and Disclosure

Material Market and Economic Conditions. March 2022-2023: Significant increases in the Federal Funds Rate by the Federal Reserve have caused REIT market prices to decline more than the broader markets. REITs rely on debt financing to acquire properties and fund their operations; expiring lower-cost debt is being refinanced at higher interest rates due to prevailing market conditions. March 2020: REIT Total Return’s value declined substantially as COVID shut down the economy. It recovered in 2021 as the economy reopened. January 2019: Tax-loss selling’s calendar expired and the government reopened on January 25, 2019. The combined effect caused our shares to rise more than the broader markets. December 2018: Another Fed-Funds rate hike, unresolved US-Chinese trade, a partial government shutdown, and an exaggerated tax-loss selling season put extreme downward pressure on equity prices. All of these factors contributed to diminished liquidity and more significant share price declines in small-cap/value issues; REIT Total Return is focused on small-cap/value issues, so our decline was significantly more precipitous.

Material Conditions, Objectives, and Investment Strategies. REIT Total Return is an actively managed investment portfolio of real estate equities, primarily common and preferred shares of REITs, with an aim to generate high total returns from a mix of dividends and capital appreciation.

All REIT Total Return Portfolio performance information on this page is based on the performance of the Portfolio Manager’s account, using the manager’s own funds. Performance of the Portfolio Manager's account is calculated by Interactive Broker on a daily time-weighted basis, including cash, dividends and earnings distributions, and reflects the deduction of broker commissions (when commissions were charged). Actual client returns will differ. **2nd Market Capital’s advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

None of the performance information displayed on this page is based on the actual performance of any 2MCAC client account investing in this portfolio. The performance in a 2MCAC client account investing in this portfolio may differ (i.e., be lower or higher) from the performance of the account managing this portfolio and portrayed on this page based on a variety of factors, such as trading restrictions imposed by the client (resulting in different account holdings), time of initial investment, amount of investment, frequency and size of cash flows in and out of the client account, applicable brokerage commissions (when commissions were charged), and different corporate actions. Clients investing in this portfolio may view the actual performance of their investment in this portfolio by logging into their Interactive Brokers account and reviewing their customized dashboard.

Clients may restrict any of the securities traded in their account but should note that any restrictions they place on their investments could affect the performance of their account leading it to perform differently, worse or better, than (a) the above-portrayed account or (b) other client accounts invested in the same portfolio.

Forward-looking statements. Commentary may contain forward-looking statements which are by definition uncertain. Actual results may differ materially from our forecasts or estimations, and 2MCAC cannot be held liable for the use of and reliance upon the opinions, estimates, forecasts, and findings in these documents.

Past performance does not guarantee future results. Investing in publicly held securities is speculative and involves risk, including the possible loss of principal. Historical returns should not be used as the primary basis for investment decisions. Although the statements of fact and data in this commentary have been obtained from sources believed to be reliable, 2MCAC does not guarantee their accuracy and assumes no liability or responsibility for any omissions/errors.

Use of Leverage or Margin. REIT Total Return Portfolio will utilize margin only for trading purposes (the ability to use the proceeds from stock sales immediately for new purchases instead of waiting for settlement), but not for borrowing purposes.

Benchmark Comparison. Our REIT Total Return Portfolio is compared to the Dow Jones Equity REIT Index and the MSCI U.S. REIT index because they are common REIT Indices. The Dow Jones Equity All REIT Index is designed to measure all publicly traded equity real estate investment trusts (REITs) in the Dow Jones U.S. stock universe. The MSCI US REIT Index is comprised of equity real estate investment trusts (REITs) eligible included within the eight Equity REIT Sub-Industries of the Equity Real Estate Investment Trust (REITs) Industry. It is not possible to invest directly in the Dow Jones Equity All REIT Index or MSCI US REIT index. Index returns do not represent the results of actual trading of investible assets/securities. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the securities underlying the index. The imposition of these fees and charges would cause the actual performance of the securities to be lower than the Index performance shown. The results portrayed include dividend income. Our REIT Total Return Portfolio may include REITs that are not eligible for inclusion in the Dow Jones Equity All REIT Index or MSCI US REIT Index.

There can be no assurance that a benchmark will remain appropriate over time and 2MCAC will periodically review the benchmark’s appropriateness and decide to use other benchmarks if appropriate.

Expenses. Returns reflect the deduction of any transaction expenses. REIT Total Return's advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

Calculation Methodology. Returns are calculated by 2MC with data from Interactive Brokers LLC using the Modified Dietz method, a time-weighted measure of performance in which cash flows are weighted based on their timing. Dividends in REIT Total Return are reinvested.

S&P Global Market Intelligence LLC. Contains copyrighted material distributed under license from S&P.