REIT Total Return Portfolio Review Heading Into 4Q23

- FFO is fine, growing moderately heading into 2024.

- Fundamental supply and demand is favorable in some sectors and unfavorable in others, which is almost always the case.

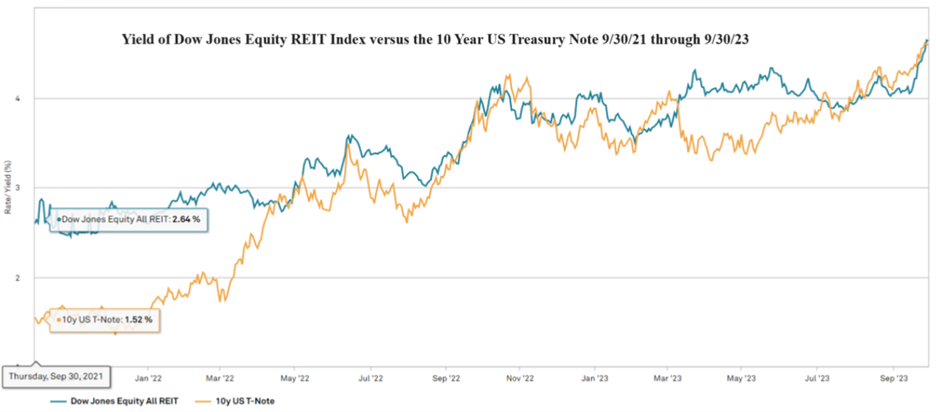

The situation is more or less normal in terms of business and earnings at a time when the pricing action of the stocks is quite abnormal. This abnormality is predicated on the rapid and large move in treasury yields and an antiquated view of REITs as yield-only plays.

REITs are not bonds and yet they have traded like fixed-income instruments trading in lockstep with the 10-year U.S. treasury. Therein lies the opportunity.

In the yield-driven selloff, fundamentals have been overlooked. The market should price in growth, but it isn’t. Some REITs can be bought at prices that correspond only to their current yield and the growth that comes with the REIT is attainable functionally for free.

In this environment, we have pivoted toward growthier sectors and growthier individual stocks because right now the marginal cost of growth in REITs is so low. It affords the wacky situation in which we can have a growth portfolio with a forward FFO multiple of 10.8X.

This 9.24% FFO yield is attainable for 2 reasons:

- REITs in general have gotten cheap with the index now trading at a 7.12% FFO yield.

- Significant mispricing within real estate sectors affords getting into growth sectors at highly discounted multiples.

Here is how our portfolio stacks up against the index.

Performance

2nd Market Capital’s REIT Total Return Portfolio (RTR) commenced trading on 7/1/16 with $100,000. Since then, no money has been added or removed which makes the current dollar value of the portfolio a really easy way to calculate cumulative performance.

Closing 9/30/23 with a value of $147,275 represents a total return since inception of 47.28%. While it is not a particularly exciting absolute return, I think it is worth noting that this was a historically bad REIT market.

From inception on 7/1/16 through 9/30/23, RTR returned 47.28% compared to the MSCI U.S. REIT index (RMS) which returned 18.10%. Over the last 5 years ending 9/30/23 we returned 12.84% compared to 14.89% for the index and over last year we returned 4.85% compared to 3.18% for the index.

Through maneuvering in and out of different property sectors and avoiding some of the pitfalls we were able to see coming we managed to stay afloat and deliver a moderate return during the dark times. It really wasn’t anything fancy, just hard work and constant alertness whenever the market is open.

Investing is a long process. It involves good cycles and bad cycles. Surviving through the hard market sets us up well to slingshot in the eventual recovery. These past 7 years have been anomalously bad in the REIT sector that over the long run has produced great returns.

The now higher interest rate environment is much healthier for REITs than the zero-interest rate atrocity.

There has been some pain in rising rates to get to the healthy zone, but now that we are here the forward outlook should be strong. Going forward, we will work hard with an intent to continue to outperform the REIT index. Based on the fundamental setup, the base index return should be significantly higher – more in line with the long-run history.

Going forward

There are a number of REITs right now that are opportunistically priced but not yet in RTR. The challenge is going to be figuring out what to sell to get the new opportunities. It will come down to relative value – which stocks provide the highest expected return relative to risk. It is an ongoing assessment and as superior value becomes available, we will try to trade into it. Good stocks should be replaced with great stocks.

Evolving economies create opportunity

Our REIT Total Return Portfolio is actively managed to pivot into wherever the opportunity is greatest. We are now offering portfolio mirroring in which the trades in our REIT Total Return Portfolio are automatically executed in client portfolios simultaneously and at the same price.

Important Notes and Disclosure

Material Market and Economic Conditions. March 2022-2023: Significant increases in the Federal Funds Rate by the Federal Reserve have caused REIT market prices to decline more than the broader markets. REITs rely on debt financing to acquire properties and fund their operations; expiring lower-cost debt is being refinanced at higher interest rates due to prevailing market conditions. March 2020: REIT Total Return’s value declined substantially as COVID shut down the economy. It recovered in 2021 as the economy reopened. January 2019: Tax-loss selling’s calendar expired and the government reopened on January 25, 2019. The combined effect caused our shares to rise more than the broader markets. December 2018: Another Fed-Funds rate hike, unresolved US-Chinese trade, a partial government shutdown, and an exaggerated tax-loss selling season put extreme downward pressure on equity prices. All of these factors contributed to diminished liquidity and more significant share price declines in small-cap/value issues; REIT Total Return is focused on small-cap/value issues, so our decline was significantly more precipitous.

Material Conditions, Objectives, and Investment Strategies. REIT Total Return is an actively managed investment portfolio of real estate equities, primarily common and preferred shares of REITs, with an aim to generate high total returns from a mix of dividends and capital appreciation.

All REIT Total Return Portfolio performance information on this page is based on the performance of the Portfolio Manager’s account, using the manager’s own funds. Performance of the Portfolio Manager's account is calculated by Interactive Broker on a daily time-weighted basis, including cash, dividends and earnings distributions, and reflects the deduction of broker commissions (when commissions were charged). Actual client returns will differ. **2nd Market Capital’s advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

None of the performance information displayed on this page is based on the actual performance of any 2MCAC client account investing in this portfolio. The performance in a 2MCAC client account investing in this portfolio may differ (i.e., be lower or higher) from the performance of the account managing this portfolio and portrayed on this page based on a variety of factors, such as trading restrictions imposed by the client (resulting in different account holdings), time of initial investment, amount of investment, frequency and size of cash flows in and out of the client account, applicable brokerage commissions (when commissions were charged), and different corporate actions. Clients investing in this portfolio may view the actual performance of their investment in this portfolio by logging into their Interactive Brokers account and reviewing their customized dashboard.

Clients may restrict any of the securities traded in their account but should note that any restrictions they place on their investments could affect the performance of their account leading it to perform differently, worse or better, than (a) the above-portrayed account or (b) other client accounts invested in the same portfolio.

Forward-looking statements. Commentary may contain forward-looking statements which are by definition uncertain. Actual results may differ materially from our forecasts or estimations, and 2MCAC cannot be held liable for the use of and reliance upon the opinions, estimates, forecasts, and findings in these documents.

Past performance does not guarantee future results. Investing in publicly held securities is speculative and involves risk, including the possible loss of principal. Historical returns should not be used as the primary basis for investment decisions. Although the statements of fact and data in this commentary have been obtained from sources believed to be reliable, 2MCAC does not guarantee their accuracy and assumes no liability or responsibility for any omissions/errors.

Use of Leverage or Margin. REIT Total Return Portfolio will utilize margin only for trading purposes (the ability to use the proceeds from stock sales immediately for new purchases instead of waiting for settlement), but not for borrowing purposes.

Benchmark Comparison. Our REIT Total Return Portfolio is compared to the Dow Jones Equity REIT Index and the MSCI U.S. REIT index because they are common REIT Indices. The Dow Jones Equity All REIT Index is designed to measure all publicly traded equity real estate investment trusts (REITs) in the Dow Jones U.S. stock universe. The MSCI US REIT Index is comprised of equity real estate investment trusts (REITs) eligible included within the eight Equity REIT Sub-Industries of the Equity Real Estate Investment Trust (REITs) Industry. It is not possible to invest directly in the Dow Jones Equity All REIT Index or MSCI US REIT index. Index returns do not represent the results of actual trading of investible assets/securities. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the securities underlying the index. The imposition of these fees and charges would cause the actual performance of the securities to be lower than the Index performance shown. The results portrayed include dividend income. Our REIT Total Return Portfolio may include REITs that are not eligible for inclusion in the Dow Jones Equity All REIT Index or MSCI US REIT Index.

There can be no assurance that a benchmark will remain appropriate over time and 2MCAC will periodically review the benchmark’s appropriateness and decide to use other benchmarks if appropriate.

Expenses. Returns reflect the deduction of any transaction expenses. REIT Total Return's advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

Calculation Methodology. Returns are calculated by 2MC with data from Interactive Brokers LLC using the Modified Dietz method, a time-weighted measure of performance in which cash flows are weighted based on their timing. Dividends in REIT Total Return are reinvested.

S&P Global Market Intelligence LLC. Contains copyrighted material distributed under license from S&P.